Article

Commentary: The Perfect (though not necessarily soft) Landing

The Perfect (though not necessarily soft) Landing — A Commentary by Nancy Tengler

By Nancy Tengler, CEO & Chief Investment Officer

A little over a week ago, during a routine Tahoe hike, I executed a perfect face plant. It’s true. I landed on my nose which landed on a slab of granite. The doctor told me my nose served as an airbag protecting the rest of my face. Yes, the snout was broken—shattered may have been the word he used—but the eye sockets, my jaw, teeth—were all intact. They stitched me up, waited for the swelling to go down and on Friday he reset the bent beak and I am back in business.

Last week I learned a perfect landing is possible. If not somewhat painful. Will that be possible for the U.S economy?

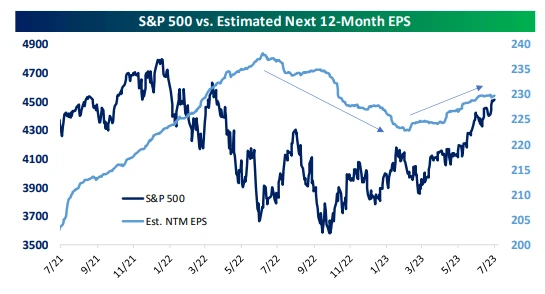

Inflation is dropping like a rock, and we are nine months into a new bull market. Thanks to Don Rismiller’s work we have pointed out for a year that inflation rises and falls in a mostly symmetrical manner, and that we hit peak inflation peak in June of 2022 when CPI breached the 9% summit. Ten months ago, our logic concluded that if inflation peaked in June, the Fed was closer to the end of the rate hike cycle than the beginning. We believed that was bullish for stocks. Many were hiding in defensive names (and still are). But we continue to like this risk-on rally (which is not to say there won’t be volatility —we would buy the dips) in technology, industrials, energy and sections of consumer discretionary for many reasons including the most important: earnings estimates are on the rise.

Bespoke Investment Group, July 21, 2023

As our old friend Larry Kudlow says: earnings are the mother’s milk of stocks. With the rally so far mostly due to multiple expansion, rising earnings estimates are needed to drive stocks further and sustainably.

(BTW: many are arguing that the rally is not reliable since only 7 or 8 stocks have driven this bull—no breadth. But it is important to note that 80% of stocks just traded above their 50-day moving average for the first time this year. The rally is widening out.)

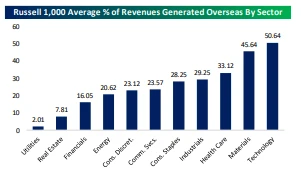

**$$$: **The sell-off in the dollar since the fall is a further tailwind to multi-national earnings. A weaker dollar improves earnings as overseas sales are repatriated to the US at a lower exchange rate.

Source: Bespoke Investment Group, July 21, 2023

Technology, materials and industrials are major beneficiaries of a weaker dollar.

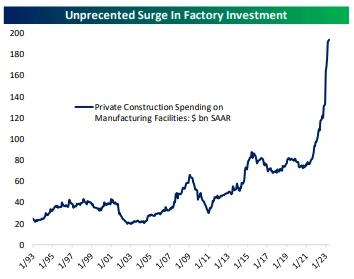

**Trillions in infrastructure spending can go a long way. **The May year over year increase in U.S. factory construction is76.3% and has more than doubled over the past two years. We are in early days of spending from the infrastructure bill and Inflation Reduction Act. Not to mention all the green energy spending allocations yet to be doled out. The implications for economic growth are meaningful and the multiplier on manufacturing jobs and construction jobs is 3-4x.

Source: Bespoke Investment Group, July 21, 2023

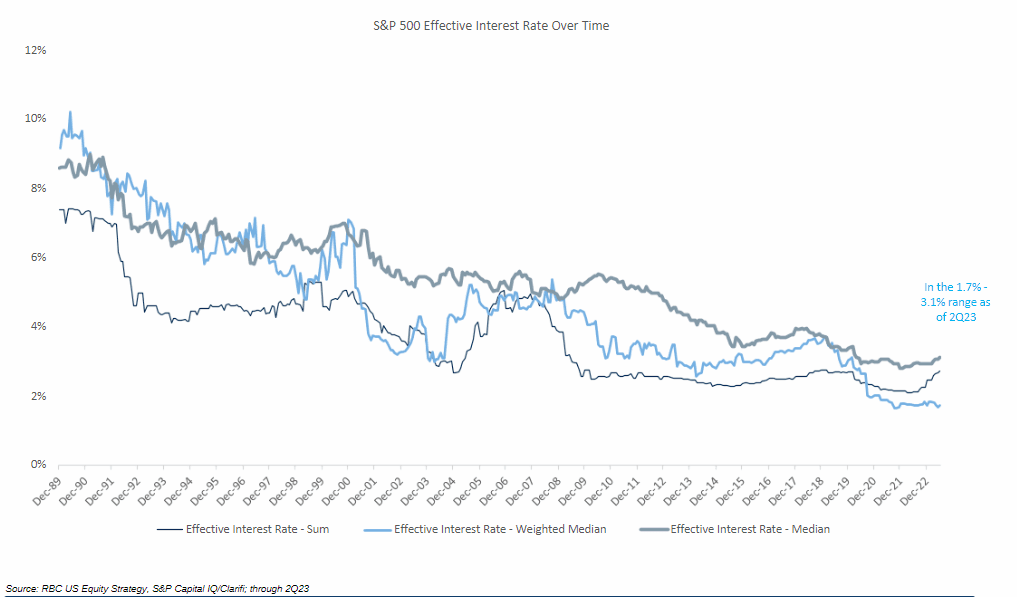

**Of course, there are plenty of indicators flashing recession—the most complex investing environment in my career to be sure. **It is important to remember that this is not a credit driven slowdown, but a self-inflicted inflation exacerbated slowdown spurred by profligate fiscal policy and monetary policy missteps. This may explain why some of the tried-and-true recession indicators have yet to result in a recession.

Also, it is possible the punch of rising interest rates has been mitigated by consumers and corporations benefiting from decades of low interest rates. Corporations had plenty of time to finance debt in the era of zero interest rates. And they took advantage. Balance sheets are solid and debt servicing levels are low. And according to yahoo!finance, 91.8% of U.S. homeowners with mortgages have an interest rate below 6% (mid-June 2023). 62% have a sub-4% rate according to Redfin and just about 25% of homeowners have a mortgage rate below 3%. In other words, the long and variable lags of monetary policy have less effect if consumers and businesses are not borrowing at the higher rates.

Source: RBC Capital Markets, July 30, 2023

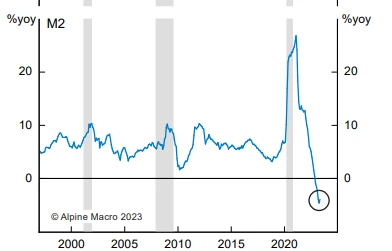

The yield curve is inverted, leading economic indicators have declined for 15 straight months and money supply has contracted after years of expansion. In our view, a restrictive signal. But after all the distortions of COVID fiscal and monetary policies it is difficult to rely on historical signals. OR, as some have argued maybe the recession has already occurred. Perhaps it is a rolling recession or a mild, not yet detectable recession.

Source: Alpine Macro, July, 17, 2023

**Soft landing? Hard landing? The perfect landing? **No one knows. But it doesn’t stop the pundits from spilling ink and consuming airtime speculating and opining. I am not sure it matters. Companies have surprised Wall Street again this earnings season. Revenues and earnings are surprising to the upside more than not and even margins are showing signs of life. With PPI (the input costs) having led CPI up and (now) down, savvy management teams are preserving and even expanding margins modestly.

It is just possible that the economy stuck the perfect landing. Or may still land. As I learned this past week, the perfect landing may not be without pain--but it may be as good as we get. And that may be enough.

Note: We are

Nancy Tengler

CEO and Chief Investment Officer

Disclosure: Laffer Tengler Investments, Inc. (“Laffer Tengler”) is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC or state securities authority does not imply a certain level of skill or training. More information about Laffer Tengler can be found on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov. Videos may discuss performance, limited to a partial list of strategies offered by Laffer Tengler Investments, and a limited list of securities that are held in client portfolios. The strategies discussed are not representative of all the strategies offered, nor do they represent all securities owned in strategies recommended by Laffer Tengler Investments.

The comments expressed represent the personal views of Laffer Tengler’s investment professionals based on their broad investment knowledge, experience, research, and analysis. The comments are not specific advice tailored to the specific circumstances of a particular individual. The comments are general and for informational purposes only, based on information and conditions prevalent at the time of publication, and are subject to change without notice due to changes in the market or economic conditions that may not necessarily come to pass. Forward-looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security, nor is this financial advice or an offer to sell any product. Viewers should not consider or place specific reliance on the content presented as comprehensive advice nor as an offer or solicitation to buy or sell securities.

Do not use this information solely when making investment decisions nor select an asset class or investment product on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs, and investment time horizon. There can be no guarantee that any listed objective is achievable nor assurance that any specific investment will be profitable. Laffer Tengler does not undertake to advise you of any change in its opinions or the information contained in this appearance. Different types of investments involve varying degrees of risk, and there is no guarantee that a portfolio will achieve its investment objective. Always consult a financial, tax, and/or legal professional regarding your specific situation. Past performance is no indication or guarantee of future results.

Laffer Tengler does not control and has not independently verified data provided by third parties, including the data, charts, and graphs presented in this appearance. While we believe the information presented is reliable, Laffer Tengler makes no representation or warranty concerning the accuracy or completeness of any data presented herein.

Latest Insights

Tengler on CNBC’s Morning Call Sheet — July 23, 2026

Nancy Tengler joins CNBC’s Morning Call Sheet to discuss how AI spending is broadening opportunities beyond Big Tech.

Tengler on Fox Business’s The Claman Countdown (July 17, 2026)

Nancy Tengler joins Liz Claman on Fox Business’s The Claman Countdown for a conversation on the market and recent semiconductor volatility.

Tengler on Yahoo Finance’s Opening Bid with Brian Sozzi (July 16, 2026)

Nancy Tengler joins Yahoo Finance’s Opening Bid with Brian Sozzi to discuss the SpaceX IPO and the case for investing in innovation.

Tengler joins Larry Kudlow on WABC with David Bahnsen (July 11, 2026)

Nancy Tengler joins Larry Kudlow on WABC with David Bahnsen for a conversation on the stock market and more.

Tengler on Bloomberg Tech (July 10, 2026)

Nancy Tengler joins Bloomberg Tech to discuss the markets and technology investing.

Tengler on Bloomberg’s Open Interest (July 6, 2026)

Nancy Tengler joins Bloomberg’s Open Interest to discuss the AI trade and the broader market setup.