Article

Commentary: “Faith is taking the first step even when you don’t see the whole staircase.” - Martin Luther King Jr.

January 15, 2024. For years I taught at St. Mary’s College in Moraga, California (where I received my MFA).

By Nancy Tengler, CEO & Chief Investment Officer

January 15, 2024. For years I taught at St. Mary’s College in Moraga, California (where I received my MFA). One of my favorite sections of the advanced composition syllabus was the persuasive essay. I always chose Dr. King’s Letter From Birmingham Jail, a literary and moral masterpiece. It never fails to delight and challenge. So, today we honor and remember Dr. King — even in a commentary on the markets — for his courage and moral clarity. His determination and kindness. And his wisdom.

Markets rebounded dramatically in 2023, what next? It is important to put last year’s robust returns into context. When looked at over two years, the S&P 500 produced a total return of 3.4%, the NASDAQ composite is down –2.4% and the DJIA is up 8.2%. This is hardly a frothy market. Following previous bear markets, the average gain in the following two years is approximately 60%. When measured from the October 2022 lows, the S&P is up 32%. This bodes well for stock returns in 2024 (though we may have to wait until the back half of the year).

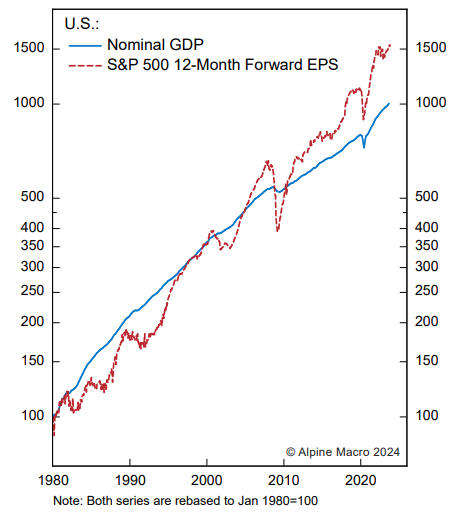

Earnings growth is on the mend—projected to come in between 10-12%--even as economic growth is expected to slow. The bears suggest that a slowing economy will reduce company pricing power and, therefore, earnings. They forget about corporate leverage. As the chart below shows, earnings have outgrown nominal GDP by more than 55% since 1980. But they are, it should be noted, notoriously more volatile.

Source: Alpine Macro, January 8, 2024

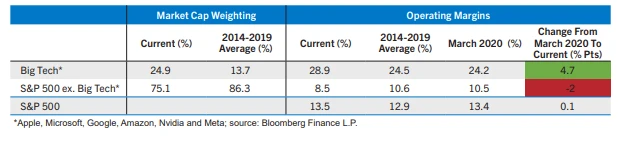

Why Technology stocks can continue to perform—they are the new defensive names. For at least the third time in the last three years strategists and commentators have declared the end to the tech trade. While we have said repeatedly all tech stocks are not created equal (in other words some segments of tech are strategically stronger than others) we have also advocated our theme of buying old economy companies who are pivoting to digital, cloud computing and generative AI technologies and the suppliers of the picks and shovels needed to succeed.

Tech margins remain impervious. And, although the forward p/e for tech is 7 points higher than the S&P 500 it remains at the low end of range over the past decade. Revenues, earnings and margins are growing much faster than the rest of the market and the secular tailwind behind cloud computing and generative AI should be respected.

Source: Alpine Macro, December 28, 2023

Technology spending is 50% of capital spending and according to Ed Yardeni is becoming increasingly less interest-rate sensitive. We would agree and have argued that when labor is tight, companies spend on technology to increase productivity. We have further argued that this market and economy are analogous to the 1990s when we were not only alive but managing billions of dollars. Above trend inflation, geopolitical shock, higher than current interest rates on the 10-year, a labor shortage, an inverted yield curve, a soft landing and improving productivity as well as share buybacks (see below) were hallmarks of the 90s. So were robust stock returns. North of 400% returns for the DJIA and S&P 500 and greater than 800% cumulative return for the NASDAQ were realized during the 1990s

Fortress balance sheets. According to The Wall Street Journal, Amazon and Alphabet enjoy a combined $18 billion in cash. Investor's Business Daily reports that the 13 non-financial companies in the S&P are sitting on cash and investments of more than $1 trillion. Most of these companies are technology companies with Microsoft holding the largest cash pile of $136.6 billion. Never mind the free cash flow these companies produce. AMZN is set to grow FCF by 66% in 2024 and earnings per share by 36%.

In a slowing economy growing earnings and free cash flow plus a strong balance sheet collecting high levels of interest are the best defense.

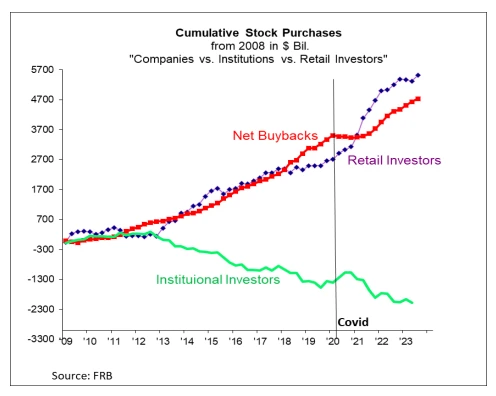

Share buybacks will rule the market in 2024. We have argued that share buybacks will put a floor under stock prices in 2024 and, most specifically, tech stocks. The shadow banking system (tip of the hat to Paul McCulley) took off in the 1990s. The shadow banking system is comprised of financial intermediaries who create credit but are not subject to bank regulatory oversight and provide flexibility to corporations trying to manage their balance sheets. Think: hedge funds, money market funds, and private credit to name a few. The credit is gobbled up by public pension plans and insurance companies who seem to have an insatiable appetite for bonds.

In the 1990s companies discovered ways (in a higher interest rate environment) to rejigger and improve their balance sheets. They also took the opportunity to return capital to shareholders via share buybacks. My partners and I debated the legitimacy and implications of buybacks in the nascent days. Whether we “believed” in them or not buybacks drove stock prices. As they continue to do today.

(Oh, and if the institutional investors graphed above ever become bullish, get out of the way!)

Recently Randy Quarles former member of the Federal Reserve remarked: “Requiring more capital will almost always improve the stability of the banking system, but it may not improve the stability of the financial system as a whole.” He says this because lending has already been taken out of the commercial banking system into the unregulated shadow banking system. Stay tuned.

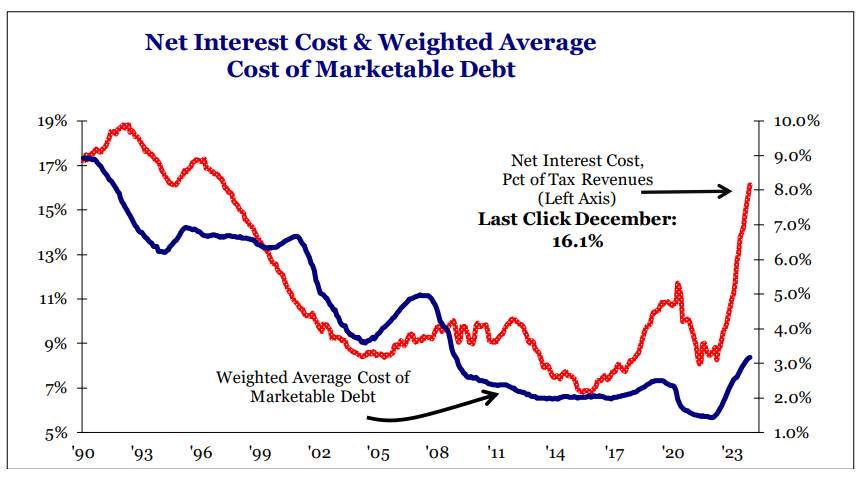

The Federal Reserve reported a loss of $114B in 2023. The chart below shows why. We have been writing about this for some time. The weighted average cost of government debt is rising pushing the net interest cost of marketable debt to over 16% of tax revenues. The losses are likely to remain robust as long as short- term rates remain high. It is important to note that the Fed issues an IOU called a deferred asset ($133B so far) to cover the deficit. Over the 109-year history of the Fed there has never been a meaningful period of suspended losses. Still, the losses continue until rates decline to around 3.5%. An incentive for the Fed to ease at some point during the first half.

Source: Strategas, January 10, 2024

Higher levels of government debt will eventually suck capital out of the private market but so far, we have not seen any signs of this.

A commentary without discussing inflation is like a day without sunshine. Sticky inflation remains elevated but rents (a significant component of CPI) are rolling over, finally. (Rents lag home prices—which are not included in CPI—by roughly one-year.) Inflation expectations have come down in various surveys, which is encouraging, and wages have come in as the labor market softens somewhat.

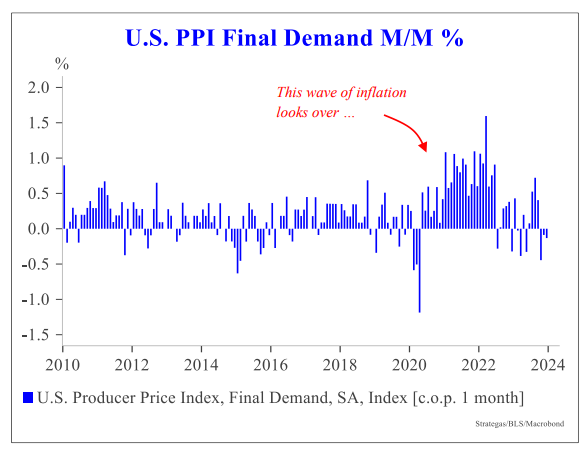

The big worry is that inflation has historically tended to come in multiple waves and the pattern—so far—is tracking previous periods. But this does not mean inflation will reaccelerate, though we are watching. The conflict in the Red Sea is providing surprisingly little upward pressure on oil but extended delivery times as shippers are forced to choose alternate routes could snarl supply chains once again. Still we take heart in the decline in PPI which led the improvements in CPI for most of last year. Anchored inflation is the key component necessary for a soft landing. We are watching.

Source: Strategas, January 12, 2024

The LTI team continues to ascend the staircase despite limited visibility. And we continue to position our portfolios according to our view that the economy is decelerating some and we want to own companies with strong free cash flow, fortress balance sheets, improving margins and sustainable top line growth. Reach out to the team if you would like to discuss any of these points further.

Nancy Tengler

CEO and Chief Investment Officer

Disclosure: Laffer Tengler Investments, Inc. (“Laffer Tengler”) is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC or state securities authority does not imply a certain level of skill or training. More information about Laffer Tengler can be found on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov. Videos may discuss performance, limited to a partial list of strategies offered by Laffer Tengler Investments, and a limited list of securities that are held in client portfolios. The strategies discussed are not representative of all the strategies offered, nor do they represent all securities owned in strategies recommended by Laffer Tengler Investments.

The comments expressed represent the personal views of Laffer Tengler’s investment professionals based on their broad investment knowledge, experience, research, and analysis. The comments are not specific advice tailored to the specific circumstances of a particular individual. The comments are general and for informational purposes only, based on information and conditions prevalent at the time of publication, and are subject to change without notice due to changes in the market or economic conditions that may not necessarily come to pass. Forward-looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security, nor is this financial advice or an offer to sell any product. Viewers should not consider or place specific reliance on the content presented as comprehensive advice nor as an offer or solicitation to buy or sell securities.

Do not use this information solely when making investment decisions nor select an asset class or investment product on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs, and investment time horizon. There can be no guarantee that any listed objective is achievable nor assurance that any specific investment will be profitable. Laffer Tengler does not undertake to advise you of any change in its opinions or the information contained in this appearance. Different types of investments involve varying degrees of risk, and there is no guarantee that a portfolio will achieve its investment objective. Always consult a financial, tax, and/or legal professional regarding your specific situation. Past performance is no indication or guarantee of future results.

Laffer Tengler does not control and has not independently verified data provided by third parties, including the data, charts, and graphs presented in this appearance. While we believe the information presented is reliable, Laffer Tengler makes no representation or warranty concerning the accuracy or completeness of any data presented herein.

Latest Insights

Tengler on CNBC’s Morning Call Sheet — July 23, 2026

Nancy Tengler joins CNBC’s Morning Call Sheet to discuss how AI spending is broadening opportunities beyond Big Tech.

Tengler on Fox Business’s The Claman Countdown (July 17, 2026)

Nancy Tengler joins Liz Claman on Fox Business’s The Claman Countdown for a conversation on the market and recent semiconductor volatility.

Tengler on Yahoo Finance’s Opening Bid with Brian Sozzi (July 16, 2026)

Nancy Tengler joins Yahoo Finance’s Opening Bid with Brian Sozzi to discuss the SpaceX IPO and the case for investing in innovation.

Tengler joins Larry Kudlow on WABC with David Bahnsen (July 11, 2026)

Nancy Tengler joins Larry Kudlow on WABC with David Bahnsen for a conversation on the stock market and more.

Tengler on Bloomberg Tech (July 10, 2026)

Nancy Tengler joins Bloomberg Tech to discuss the markets and technology investing.

Tengler on Bloomberg’s Open Interest (July 6, 2026)

Nancy Tengler joins Bloomberg’s Open Interest to discuss the AI trade and the broader market setup.