Article

Commentary: What Could Go Right in 2023?

Nancy Tengler Commentary: What Could Go Right in 2023? Sentiment will shift at some point; we want to be ahead of the pack.

By Nancy Tengler, CEO & Chief Investment Officer

Sentiment will shift at some point; we want to be ahead of the pack.

Warren Buffett has said many clever things over the decades. But the following is one of my favorites: “In the business world, the rearview mirror is always clearer than the windshield.” In other words, the past is crystal clear. The future? Not so much. That is why at turning points so many investors stay too long at bull market parties and bail out when bear market routs become too much to bear (pun not intended).

I know I will offend every technical, engineering-focused mind who reads this, but in my experience, investing is about being mostly right. (Yes, I know, I know, you can’t build a bridge by being mostly right!) An important investing skill lies in sensing when to pivot. While it is nearly impossible to bottom tick the stock market—getting it mostly right can be a victory that pays off in subsequent years. If an investor buys a stock at $100 and it declines to $80 shortly thereafter but hits $300 a few years later, the best question to ask, perhaps, is why that investor didn’t buy more. Not why did he buy the stock at all.

We think investors have become way too pessimistic given where we are in the rate hiking cycle. Since March the Fed has raised rates 4.25%--one of the fastest rate hiking regimes in history. And, because monetary policy has a lagged effect on the economy, we expect the economy to slow materially or enter recession at some point in 2023. To be sure a severe recession would be bearish for stocks, yet given the resilience of the U.S. economy and the tight labor market, we are expecting a slowdown or shallow and brief recession. That could allow stocks to rally in the second half of 2023 (after a volatile Q1) as they look around the recession corner.

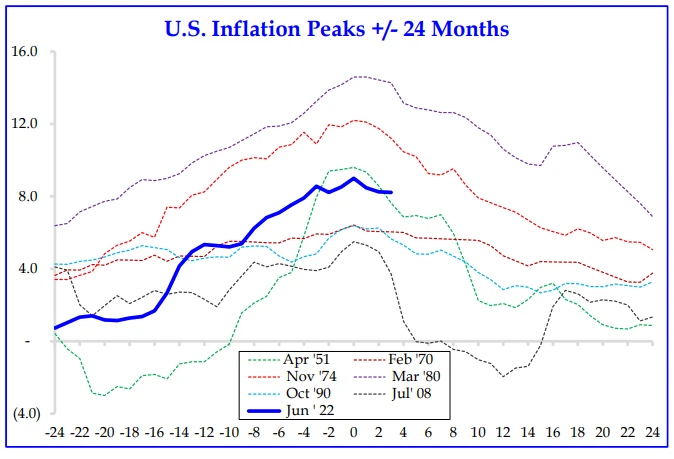

Inflation will continue to roll over. We believe inflation peaked in June. On November 2,2022, I wrote a piece “How To Make Sense Of The Columbo Economy” Link here the following:

Peak inflation and timing of Fed pause. It was our contention in the spring of 2021 that inflation would be more persistent and stickier than the Fed’s transitory view. We take no comfort in being correct. We have written that we believe peak inflation in the headline CPI was reached in June of this year when it hit 9.1%. And we believe, as history shows, that the rise and fall of inflation is mostly symmetrical. It took 16 months to peak and now we expect it will take a like amount of time to get to a tolerable level (not necessarily 2.0%–the Fed’s target).

Source: Strategas, October 19, 2022

We would emphasize that the trend is not necessarily linear as you can see in the chart above. But, inflation is, indeed, rolling over.

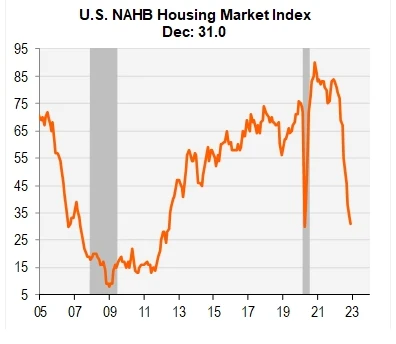

Housing is in freefall, manufacturing PMIs are in contraction, inventories are up, prices paid down, energy costs have come in, used car prices have declined materially as have airfares and hotels, wheat and corn are down, shipping costs have plummeted, copper, aluminum and palladium are well off their highs, and medical insurance costs are set to decline by –40% over the next 12 months. While we don’t think the Fed’s 2% inflation target is on the horizon, we do think inflation will surprise many to the downside.

Source: Piper Sandler December 2022

Recession likely but not deep. The inversion of the yield curve and the steady decline in Leading Economic Indicators (chart below) almost ensure we see an official recession (versus 2022’s slowdown) at some point in 2023. The question? How severe and long will the slowdown in economic growth end up being?

Source: Bloomberg, December 22, 2022

The consumer still has bandwidth and given the tight labor market we think spending will hold up better than the naysayers predict. Which is not to say it won’t slow. But generally, we think the bears (never eager to leave the stage) are too pessimistic.

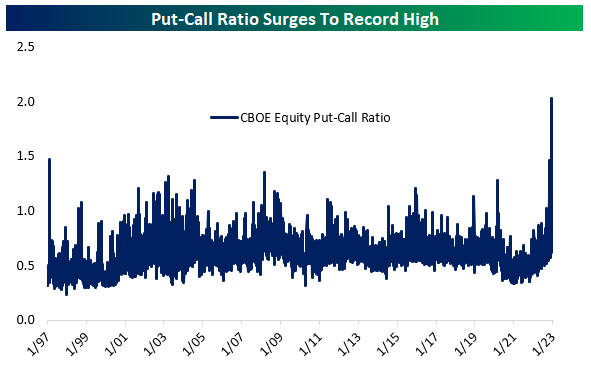

Sentiment is too negative (this is not the 1980s). Recent put volumes outnumbered call volumes by a factor of 2 on the CBOE—the highest level since the data has been measured. The move was driven by a surge in put options and a decline in call options. The put call ratio tends to be a contrary indicator spiking when investors are too pessimistic. Add to that institutional investors have remained on the sidelines with allocations to equities below levels held in 2008!

Source: Bespoke Investment Group, December 22, 2022

What are we worried about?

The omnibus bill is likely to put upward pressure on inflation just as the Fed is making progress. Another day another $1.8 trillion in spending.

The transition to onshoring/re-shoring could be a little messy but good news in the long-term. Hundreds of companies have announced their intention to move manufacturing back to the United States. Many are shifting from China to India and Vietnam.

Geopolitical tension in the South China Sea.

The Bear Market of 2023, if over, would rank as one of the mildest of the 14-prior post—World War II bear markets at 282 days. Interestingly according to our friends at Bespoke Investment Group, this bear market has experienced seven 5% rallies, three of which extended to 10%. Those facts belie the way many feel about this bear market. I have been at this a long time and the only bear market that felt worse was the one that spanned 2001-2003. Investors are exhausted. Ultimately that will bode well for stocks in 2023. Q1 could be choppy (perhaps we will see the price exhaustion indicators marking a bottom then?) but we think the returns on stocks will be positive in 2023, though not necessarily spectacular.

Beware of unintended consequences. When government inserts itself into the free market unintended consequences abound. In 2022, due to high natural gas prices (wind and solar were unable to offset lower energy production from hydro and nuclear power) global coal usage hit an all-time high according to a report by the IEA.

Here’s to a Happy and Prosperous New Year!

Nancy Tengler

CEO and Chief Investment Officer

Disclosure: Laffer Tengler Investments, Inc. (“Laffer Tengler”) is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC or state securities authority does not imply a certain level of skill or training. More information about Laffer Tengler can be found on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov. Videos may discuss performance, limited to a partial list of strategies offered by Laffer Tengler Investments, and a limited list of securities that are held in client portfolios. The strategies discussed are not representative of all the strategies offered, nor do they represent all securities owned in strategies recommended by Laffer Tengler Investments.

The comments expressed represent the personal views of Laffer Tengler’s investment professionals based on their broad investment knowledge, experience, research, and analysis. The comments are not specific advice tailored to the specific circumstances of a particular individual. The comments are general and for informational purposes only, based on information and conditions prevalent at the time of publication, and are subject to change without notice due to changes in the market or economic conditions that may not necessarily come to pass. Forward-looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security, nor is this financial advice or an offer to sell any product. Viewers should not consider or place specific reliance on the content presented as comprehensive advice nor as an offer or solicitation to buy or sell securities.

Do not use this information solely when making investment decisions nor select an asset class or investment product on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs, and investment time horizon. There can be no guarantee that any listed objective is achievable nor assurance that any specific investment will be profitable. Laffer Tengler does not undertake to advise you of any change in its opinions or the information contained in this appearance. Different types of investments involve varying degrees of risk, and there is no guarantee that a portfolio will achieve its investment objective. Always consult a financial, tax, and/or legal professional regarding your specific situation. Past performance is no indication or guarantee of future results.

Laffer Tengler does not control and has not independently verified data provided by third parties, including the data, charts, and graphs presented in this appearance. While we believe the information presented is reliable, Laffer Tengler makes no representation or warranty concerning the accuracy or completeness of any data presented herein.

Latest Insights

Tengler on CNBC’s Morning Call Sheet — July 23, 2026

Nancy Tengler joins CNBC’s Morning Call Sheet to discuss how AI spending is broadening opportunities beyond Big Tech.

Tengler on Fox Business’s The Claman Countdown (July 17, 2026)

Nancy Tengler joins Liz Claman on Fox Business’s The Claman Countdown for a conversation on the market and recent semiconductor volatility.

Tengler on Yahoo Finance’s Opening Bid with Brian Sozzi (July 16, 2026)

Nancy Tengler joins Yahoo Finance’s Opening Bid with Brian Sozzi to discuss the SpaceX IPO and the case for investing in innovation.

Tengler joins Larry Kudlow on WABC with David Bahnsen (July 11, 2026)

Nancy Tengler joins Larry Kudlow on WABC with David Bahnsen for a conversation on the stock market and more.

Tengler on Bloomberg Tech (July 10, 2026)

Nancy Tengler joins Bloomberg Tech to discuss the markets and technology investing.

Tengler on Bloomberg’s Open Interest (July 6, 2026)

Nancy Tengler joins Bloomberg’s Open Interest to discuss the AI trade and the broader market setup.